Quarterly Commentary

Market Overview

As the second quarter came to a close and we entered into the third quarter, markets continued their upward trajectory as the S&P 500 rose to its highest level since March 2022. Unfortunately, this trajectory proved unsustainable as rising global bond yields, mixed inflation data, and concerns over a future economic slowdown weighed on the major indices in August and September.

Coming into the year, it was widely predicted that a recession could kick in as soon as the second half of the year. As we moved into the third quarter, fairly robust economic data, along with declining inflation, was helping to re-write that story. The Federal Reserve, in the meantime, increased rates by 25 basis points in July yet also signaled that their rate hike cycle could be nearing an end. The Fed’s tone fueled optimism within the market. Further adding to the optimism was an earnings season that was better than expected that featured mostly favorable guidance into ’24.

Everything seemed to change in early August following the downgrade of U.S. sovereign debt by Fitch Ratings. The agency cited concerns over the government’s long-term fiscal trajectory as its reason for the downgrade. The decision was likely influenced by the debt ceiling stand-off that had played out just over a month earlier. The downgrade kickstarted a rise in Treasury yields that continued throughout the month. Adding to pressure on yields was an increase in Treasury issuance as well as some inflation data that gave investors pause. Any optimism generated the previous month had been deflated and the result was the first negative month since February for the S&P 500.

During the first half of September, it looked as though volatility from the previous month had subsided. This was not to be, however, as the Fed’s FOMC delivered comments at their September meeting that were interpreted as hawkish despite not having raised interest rates. Two late quarter developments further weighed on the markets. Those developments included the UAW labor union strikes against the “big three” auto makers and then the potential government shutdown that was averted just as the fiscal year was expiring. The agreed upon Continuing Resolution will expire on November 17th, thus kicking the can not very far down the road.

Performance

Rising bond yields were the story during the quarter as higher Treasury yields weighed on performance on a sector as well as index basis. Large-cap equities led all market capitalizations despite being negative for the quarter. The DJIA declined 1.3% in the third quarter while the S&P 500 declined 2.1%, the S&P Mid-Cap 400 declined 3.6%, and the Russell 2000 declined 4.8%.

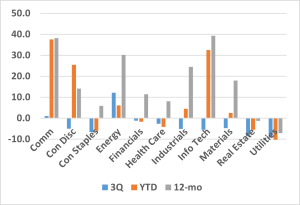

S&P 500 Sector Performance (ETF)

This performance is consistent with the notion that smaller companies will underperform as rates rise due to their greater reliance on debt financing.

From a style standpoint, there was a relative reversal from the first two quarters. Value, which is not affected by rising rates to the extent growth is affected, outperformed during the quarter though both styles were negative. At the sector level, all but two sectors were down on the quarter. On the back of surging crude oil prices, the energy sector was by far the best performer for the quarter with a gain of 12.2%. Though turning in a much more modest gain, the communications sector (+1.0%) was the only other sector in positive territory. Returning to our theme of rising bond yields, it’s not much of a surprise that utilities (-9.2%), real estate (-8.6%), and consumer staples (-6.6%) were the greatest laggards. These sectors generally offer some of the highest dividend yields, however, as bond yields rose rather quickly, those dividends became less attractive and investors subsequently rotated out of those sectors.

International

Foreign equity markets saw moderate declines for the quarter as the MSCI EAFE Index fell 3.32%. Emerging markets outperformed developed markets on a relative basis, however, they too declined over the quarter as the MSCI Emerging Market Index declined 2.48%. Foreign markets, both developed and emerging are experiencing varying degrees of recessions fears which largely explains across the board market losses. Also weighing on the market are concerns related to China’s housing market.

Commodities

The price of WTI crude seemed to be pushing toward $100/barrel prior to retreating late in the quarter. As we begin the fourth quarter, the futures market for crude is in what’s known as “backwardation”, meaning that near-term front-month prices are meaningfully higher than future prices. The premium for spot oil over futures is due to several supply and demand factors. Those factors include Saudi Arabia and its cartel partners holding down production in an effort to boost prices and a glut of oil storage capacity at the Cushing, Oklahoma trading hub where WTI is priced.

Crude Oil Prices - WTI

In other commodity markets, mining executives are warning that the world’s growing thirst for materials such as lithium, cobalt, nickel, and refined copper are at odds with an aversion to new mining projects. These materials, which are essential to the stated desire to transition away from fossil fuels, are forecast to enter a supply deficit as soon as 2027. Miners cited an overall slow permitting process, opposition to new projects and a shortage of investment in exploration as factors in the stated forecast.

Fixed Income

In fixed income, the Bloomberg Barclays US Aggregate Bond Index declined 2.9% for the quarter. The negative performance in traditional fixed income sectors can largely be attributed to rising Treasury rates amid continued hawkish sentiment from the Fed that indicated an intention to monetary policy tighter for longer.

The uptrend in Treasury yields that began in May not only continued but accelerated throughout the third quarter. Intermediate-duration and long-duration yields bore the brunt of the steepening as investors adjusted to ongoing upside surprises to growth. In the Agency MBS market, prepayment speeds slowed as expected. The decline in prepays was driven by higher mortgage rates which, in turn, lead to lower refinancing activity. In the Corporate debt market, short-duration credit was positive for the quarter (0.8%) relative to intermediate-duration (-0.9%), and long-duration (-7.2%). On the short-end, the sectors that performed well were finance companies and airlines while industrials were the laggards. In High Yield, the higher-for-longer narrative adversely impacted riskier assets. For the seventh consecutive month, September marked a higher volume of upgrades than downgrades as reported by J.P. Morgan.

Municipal bond yields moved higher over the quarter in sympathy with Treasuries. Both General Obligation and Revenue bonds produced similar returns. The yield difference or “spread” between AAA-rated and A-rated bonds have recently narrowed. The narrowing trend could continue until signs of credit deterioration appear, perhaps from a recession or a drop in federal support funding. Until either occur, investors will most likely continue to reach for yield.

Inflation

The disinflationary trend appears to be stalling if the inflation numbers are any indication. September’s producer price index (PPI) came in higher than expected, rising 0.5% versus a forecast of a 0.3% increase, while the year-over-year increase of 2.2% was the most significant jump since April. The driver of last month’s hop was in goods, which surged 0.9%.

Consumer inflation data followed, which also came in hotter than forecast. The Consumer Price Index (CPI) rose 0.4% in September and 3.7% year-over-year above the forecast of 0.3% and 3.6%, respectively. The news on core inflation was a bit more comforting, rising in line with expectations.

Consumer Price Index – YoY Change

Fourth Quarter Insights

As we move into the fourth quarter, the markets continue to navigate the effects of rising interest rates and economic uncertainty. The ongoing federal budget discussions, China’s economic slowdown, and the war in Ukraine are just a few topics that have the potential to weigh on markets. Despite what seems like an endless parade of negative headlines, there are reasons to be more optimistic than in 2022.

The first reason for optimism is that inflation has been improving relative to last year. The CPI has slowed to 3.7% on a year-over-year basis as of August compared to 8.3% for the same point in 2022. While this is still higher than the Fed prefers, the trend has been moving in the right direction and all evidence points to the FOMC’s resolve to get inflation down to its target of 2%.

A second reason to take an optimistic view is that the economy continues to grow, highlighted by the Atlanta Fed’s GDPNow estimate for 3Q still at 4.9%. It’s easy to forget that many economists predicted a recession toward the end of this year. Additionally, the unemployment rate remains fairly low at 3.8%. Despite some softening in new hires, there continues to be more job openings than unemployed workers to fill them.

Finally, the Fed appears to be nearing the end of its rate increase cycle. Over the past year, the economy has had time to adjust to what now appears to be a “higher for longer” interest rate environment. While this has the potential to present challenges for certain sectors such as real estate and technology, it also presents opportunities for investors in fixed income as yields rise.

The strategy here at Chesapeake Wealth Management related to bonds, focuses on high quality securities, across various asset classes with in the fixed income markets. Dependent upon an investors individual goals, objectives and tax brackets, the appropriate sector of the bond market should be considered carefully. As has always been the case, CWM manages all bond portfolios with a tailored approach to each individual investors’ specific needs, focusing on quality and protecting principal.

Brian T. Moore

October 2023

Disclaimer

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Chesapeake Wealth Management), or any non-investment related content, made reference to directly or indirectly in this newsletter, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Chesapeake Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his or her individual situation, he or she is encouraged to consult with the professional advisor of his or her choosing. Chesapeake Wealth Management is neither a law firm nor a Certified Public Accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the Chesapeake Financial Group, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.